5 Reasons This Isn’t a Repeat of the 2008 Housing Crash

Source: 5 Reasons This Isn’t a Repeat of the 2008 Housing Crash (nar.realtor)

Many homeowners are still haunted by the 2008 housing crash when property values collapsed and foreclosures spiked. The memory of sudden catastrophe at a time when the real estate market had been riding high may help explain why 41% of Americans say they now fear a housing crash in the next year, according to a new survey from LendingTree.

Are their fears well-founded?

“It’s a valid question,” Lawrence Yun, chief economist for the National Association of REALTORS®, said Tuesday at NAR’s Real Estate Forecast Summit. “People are remembering the crushing and painful foreclosure crisis. So, it has become a key question: Will home prices crash after the strong run-up in prices across the country over recent years?”

At the virtual conference, where leading housing economists offered their 2023 forecast for the real estate market, Yun offered assurance that current dynamics are nothing like during the Great Recession. He pointed to several key indicators of how this market differs.

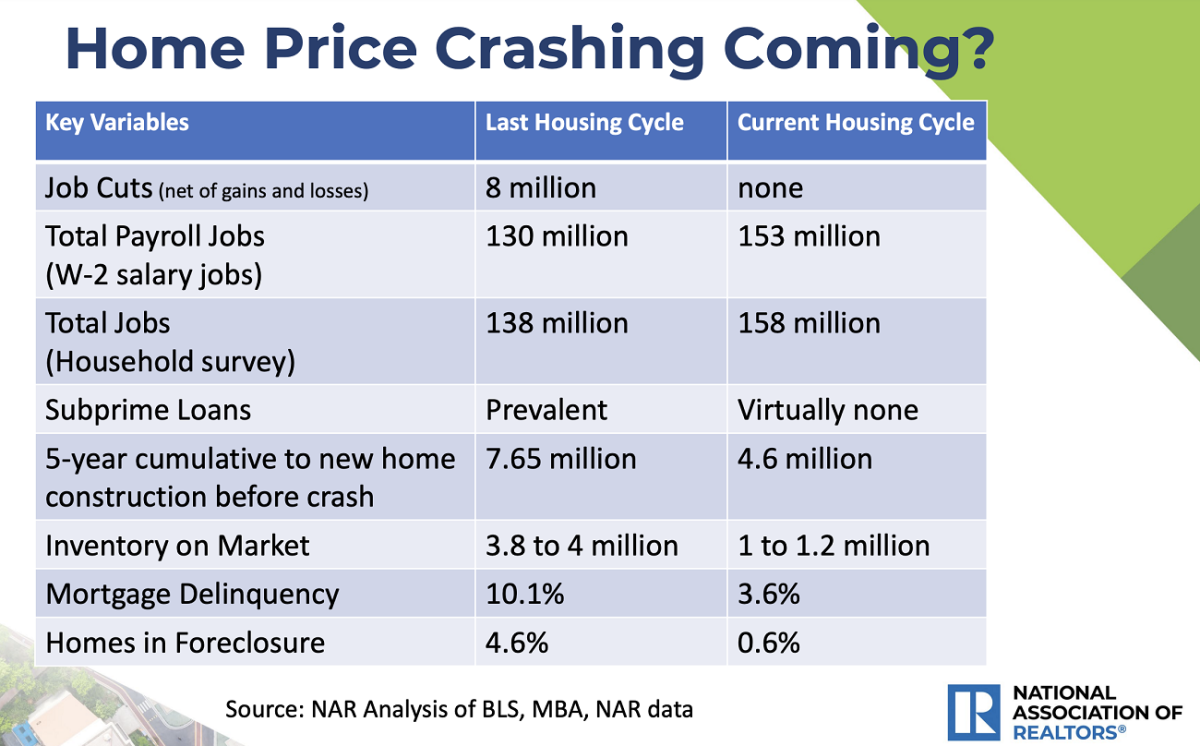

- The labor market remains strong. In the last major housing downturn, there were 8 million job losses in a single year. Now there are virtually none. Though layoffs in the technology and mortgage industries are occurring, they haven’t accumulated enough to form a net job loss, Yun noted. A strong job market bodes well for housing’s future.

- Less risky loans. Yun also noted the subprime loans that were prevalent during the 2008 housing bust are basically nonexistent today.

- Underbuilding and inventory shortages. New-home construction prior to the 2008 crash was amounting to 7.65 million units annually. Today, it’s 4.6 million. Yun points to “a massive housing shortage” from a decade of underproduction in the housing market.

- Delinquency lows. About 10% of all mortgage borrowers were delinquent on their loans in the previous housing bust. The mortgage delinquency rate is now at 3.6%, holding at historical lows, Yun said.

- Ultra-low foreclosure rates. Homes in foreclosure reached a rate of 4.6% during the last housing crash as homeowners who saw their property values plunge walked away from their loans. Today, the percentage of homes in foreclosure is 0.6%—also at historical lows, Yun said. He predicted foreclosures to remain at historical lows in 2023.

Overall, the fundamentals don’t point to a housing market that is operating similarly to the 2008 cycle, Yun said. While home sales are slowing, prices remain up nearly 6% as of October sales numbers compared to a year ago. Also, inventory remains low, which will keep home prices elevated, Yun said. “The chance of a price crash is very small due to the lack of supply.”

Melissa Dittmann Tracey is a contributing editor for REALTOR® Magazine, editor of the Styled, Staged & Sold blog, and produces a segment called “Hot or Not?(link is external)” in home design that airs on NAR’s Real Estate Today radio show. Follow Melissa on Instagram and Twitter at @housingmuse.